With Tax Day right around the corner, here are eight things you should keep in mind as you prepare your 2023 taxes. If you have any questions or need help filing your 2023 taxes Warren Accounting is here to help you.

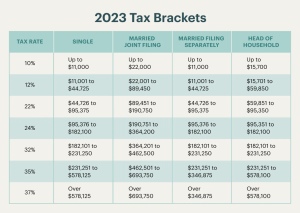

1. Income tax brackets shifted.

There are still seven tax rates (brackets) but the income ranges for each have changed slightly to account for inflation. The following tax rates and income ranges will apply for 2023.

2. Slight increase to the standard deduction.

The standard deduction increases to $13,850 for single filers and married couples filing separately. Single head of household filers, who are generally unmarried with one or more dependents, rises to $20,800. And the standard deduction for married couples filing jointly increased to $27,700.

3. The Child Tax Credit could provide a tax break.

Tax credits are normally better than deductions. Credits reduce the tax you owe dollar for dollar and deductions reduce how much of your income is subject to being taxed. The Child Tax Credit is $2,000 per child under age 17. The credit is also subject to a phase-out starting at $400,000 for joint filers and $200,000 for single filers. For other qualified dependents, you can claim a $500 credit.

4. Itemized deductions are mostly the same.

For many filers, taking the higher standard deduction saves them the hassle of keeping track of their receipts. However, if you have a large amount of tax-deductible expenses, it may be beneficial for you to itemize. The rules for itemized deductions have not changed much, but we would like to point them out.

Local & State Taxes: The deduction for state and local income taxes, property taxes, and real estate taxes is $10,000.

Mortgage Interest: The mortgage interest deduction is limited to $750,000 of indebtedness. But if you had $1,000,000 of home mortgage debt before December 16, 2017, you will still be able to deduct the interest on that loan.

Medical expenses: Medical expenses must exceed 7.5% of adjusted gross income (AGI) can be deducted in 2023.

Charitable donations: The annual income tax deduction limits for gifts to public charities are 30% of AGI for contributions of non-cash assets—if held for more than one year—and 60% of AGI for contributions of cash. If you give both can and non-cash assets, the overall limit is generally 50% of AGI.

Miscellaneous deductions: No miscellaneous itemized deductions are allowed.

5. 401(k) and IRA limits are slightly more.

Contribution limits for the traditional IRA and Roth increased slightly from 2022. Individuals can contribute up to $6,500 to an IRA. If you are age 50 and older, you qualify to make an additional $1,000 catch-up contribution. In addition, the contribution limits for tax-deferred 401(k)s and Roth 401(k)s increased to $22,500. And, if you are age 50 or older, you qualify to make an additional $7,500 catch-up contribution.

If you are in the position to do so, consider maxing out your contributions. By doing this you are boosting your retirement savings, and it could also provide a possible tax deduction.

6. You can save more in your health savings account (HSA).

The maximum contribution to an HSA is $3,850 for an individual (up $50 from 2021) and $7,750 for a family (up $100). People aged 55 and older can contribute an additional $1,000 catch-up contribution.

7. The alternative minimum tax (AMT) exemption is higher.

Until the AMT exemption enacted by the Tax Cuts and Jobs Act expires in 2025, the AMT will continue to affect mostly households with incomes over $500,000. The AMT exemptions are $81,300 for single filers and $126,500 for married taxpayers filing jointly. The phase-out thresholds are $1,156,300 for married taxpayers filing a joint return and $578,150 for all other taxpayers. (Once your income for the AMT hits the phase-out threshold, your AMT exemption begins to phase out at 25 cents for every dollar over the threshold.)

8. The estate tax exemption increased.

The estate and gift tax exemption rose to $12,920,000 for 2023. The higher exemption, set to expire at the end of 2025, could be cut in half at that time if Congress does not act.

The annual gift exclusion, which allows you to give money to your loved ones each year without incurring any tax liability or using up any of your lifetime estate and gift tax exemption, increases to $17,000 per recipient (up $1,000 from 2022).